Of Counsel

November 3, 2017

Dear Friends,

As many of you know Republicans in the U.S. House of Representatives released their proposal for federal tax reform (known as the “Tax Cuts & Jobs Act”) yesterday. Republicans in the U.S. Senate are expected to release their proposed plan next week. At FGMC we will be watching and evaluating the legislative process with regard to federal tax reform very closely and we hope to provide you with periodic updates as we learn of significant developments.

What follows is an analysis of what we have learned from yesterday’s tax proposal and how it may affect you. This analysis is only intended as a summary of those provisions likely to affect most of our clients. It is not intended to be a comprehensive review of the entire piece of proposed legislation (which is over 400 pages long). If we’ve missed an aspect of the tax plan you would like more information about, please feel free to contact me. Our summary is lengthy, but I encourage you to at least scan the headings of each section. I’m sure you will find some aspects of the proposed legislation you will be interested in.

We have not endeavored to quantify how much certain classes of Americans will save under the proposed legislation (e.g., a family of four earning x amount of dollars) since this requires consideration of a myriad of assumptions and cases. Instead and in the future we will try to pass along any useful analyses conducted by non-partisan tax policy organizations. Also, keep in mind that this information is still being digested. Sometimes it’s easy to take an initial glance at one proposed change in the law without realizing its overall impact when combined with other changes. Additionally, with a 400-page bill its possible we may have overlooked some aspects of the proposed legislation. Over the course of the legislative process we will have additional opportunities to sort through some of these details and ultimately provide you with a timely and accurate reporting of what becomes final law.

As many of you know, when it comes to taxation my personal views often do not align with either the Republicans or Democrats. As the author of these updates it is my intent to eliminate personal opinions and present an unbiased analysis of proposed legislation.

Feel free to contact me with any questions, or if you would like my take on any of the inevitable political spin either in favor or against this legislation.

Sincerely,

Steven M. Weiser, Esq.

FOSTER GRAHAM MILSTEIN & CALISHER, LLP – ANALYSIS OF THE TAX CUTS AND JOBS ACT

Individual Income Taxes

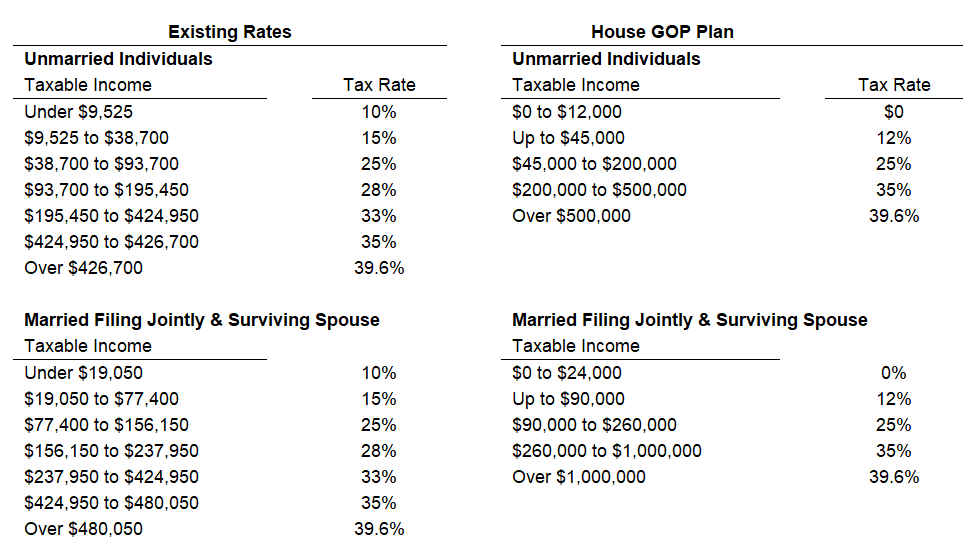

Income Tax Brackets

The Proposal: The proposed legislation reduces the number of tax brackets and enlarges the income thresholds at which each higher bracket is reached. Below is a comparison of existing brackets and those proposed for the single and married filing jointly brackets. Note, that when reviewing brackets they should be interpreted as for example “Over $9,525 but not over $38,700.” Also, brackets are progressive, so that even high earning individuals may take advantage of the lower rates on those portions of their incomes fitting into the lower tax brackets.

Analysis: This aspect of the proposed legislation should result in reduced income taxes for individuals in all tax brackets.

Individual Standard Deduction

The proposed legislation increases the standard deduction. The following is a comparison of existing law and the proposed changes for the standard deductions for those filing as unmarried persons, married filing jointly or surviving spouse, and head of household:

Analysis: For some lower earning Americans or those who do not itemize deductions the increased standard deduction provides a tax savings by way of the increased tax deduction. The House GOP represents that the increased standard deduction simplifies tax compliance by eliminating the need for many Americans to itemize (however, one would think many Americans would still go through the process of evaluating each year whether the standard deduction or itemizing deductions is more advantageous).

Personal Exemptions

The Proposal: A personal exemption deduction is allowed for taxpayers and their qualifying dependents. The amount of the deduction in 2018 is $4,150 for each such person (e.g, a married couple with two young dependents will have a $16,600 deduction). The exemption is phased out at high income levels (beginning at $320,000 for married persons filing jointly and $266,700 for single individuals). The proposed legislation eliminates the personal exemption deduction entirely.

Analysis: This proposal would seem to offset much of the benefit of an increased standard deduction for many Americans. For example, a young family of four that does not itemize exemptions has the additional standard deduction of $11,000 (when compared to existing law) offset entirely by the loss of the personal exemption and dependent deduction which is worth $16,600 in 2018. The net effect of these two changes alone may result in increased taxable income for some people in 2018. Of course considering only these two reforms without regarding to anything else, is probably not realistic for most taxpayers.

State and Local Tax Deduction

The Proposal: The proposed legislation would eliminate the ability of individuals to deduct state and local income taxes and sales taxes. It would also limit the deduction of property taxes to $10,000.

Analysis: This aspect of the proposed legislation is receiving a lot of attention. Presumably, taxpayers residing in high tax states will be burdened by this provision more than other taxpayers, because of the inability to deduct state and local income taxes, or because property taxes often exceed the $10,000 threshold, or both. I expect to see this proposal change or be eliminated from any final legislation.

Mortgage Interest Deduction

The Proposal: The deduction for home mortgage interest is retained. However, the deduction is only allowed with respect to interest paid on up to $500,000 of acquisition indebtedness, down from the current threshold of $1 million. However, interest on debt exceeding $500,000 and up to $1 million is grandfathered (the entire amount of interest is deductible) if such debt was in place prior to November 2, 2017.

Analysis: I would expect a lot of blowback on this proposal from many of those in the residential real estate industry and homeowners in areas where property values are highest. The mortgage interest deduction has long been considered significant in making home ownership affordance for many Americans, and touching this deduction may cause outrage among those who believe it might adversely impact the residential real estate market.

Deduction for Tax Preparation Expenses

The Proposal: The proposed legislation eliminates the deduction for tax preparation expenses (e.g., the cost of having your accountant prepare your annual income tax return).

Analysis: There’s not much to say about this. Tax preparation expenses can be significant for some individuals, making the cost of seeking professional assistance with tax return preparation much more affordable if a deduction is allowed.

Deduction for Alimony or Separate Maintenance

The Proposal: Currently, a taxpayer is entitled to deduct the amount of alimony or separate maintenance they are required to pay to their ex-spouse. The proposed legislation eliminates this deduction, and also eliminates the requirement that the ex-spouse recognize these payments as taxable income.

Analysis: I’d be surprised if this proposal makes it into a final bill. It would appear that from the government’s standpoint this proposal is largely revenue neutral (unless the payee is in a lower tax bracket than the payor), and merely shifts the recognition of income from one ex-spouse to the other. You might think all this accomplishes is creating additional resentment that a payor ex-spouse has for the payee ex-spouse. I’m interested to hear from my colleagues that practice family/divorce law how these modifications might affect divorce negotiations for their clients.

Deduction for Charitable Contributions

The Proposal: The proposed legislation would increase the limitation on cash contributions to public charities from 50% to 60% of a taxpayer’s adjusted gross income (AGI). Contributions in excess of these amounts may be carried forward for five years.

Analysis: Many people in the nonprofit community were concerned that this bill if passed would hinder the ability of tax-exempt organizations to raise funds. If fewer Americans itemize deductions and instead take a larger standard deduction it eliminates for many taxpayers a tax incentive to make charitable gifts. Historically I don’t often encounter individuals that have charitable contributions in excess of 50% of their AGI (or more technically speaking, their contribution base which is a slightly modified AGI). I would be surprised if increasing the deduction limitation results in a significant change to current philanthropic practices of most Americans. If this proposal was included in the House GOP’s bill to appease nonprofit organizations concerned about the increased standard deduction, I will be surprised if those goals are actually accomplished.

Child Tax Credit

The Proposal: The House GOP bill calls for a repeal of the exist Child Tax Credit and replacing that credit with a new “Family Credit.” The Child Tax Credit allowed for a credit of $1,000 for each dependent child of the taxpayer. The Family Credit increases this amount to $1,600 and also allows for a $300 credit, beginning January 1, 2023 for each parent and other qualifying dependent of the taxpayer. The credit is phased out for married couples filing jointly when income exceeds $230,000 (up from $110,000 under current law), and for other filers when income exceeds $115,000 (up from $75,000 under current law).

Analysis: This change is intended to benefit low and middle income taxpayers the most. By raising the phase-out threshold significantly, more Americans will benefit.

Other Tax Credits

The Proposal: The proposed legislation also repeals tax credits for the elderly and totally permanently disabled (IRC § 22), adoption expenses (IRC § 23), and the credit for qualifying plug-in electric vehicles (IRC § 30D).

529 Accounts

The Proposal: The rules governing 529 Plans will be modified under the proposed legislation to allow for the distribution, on a tax-free basis, of up to $10,000 for elementary and secondary school tuition. Currently, tax-free distributions are only allowed for qualifying higher education expenses (college level and above).

Analysis: This is sure to be popular among Americans sending their children to private school. This proposal would allow parents to tap into funds already set aside, and increase opportunities to save for such tuition on a tax free basis. An additional benefit is a potential state income tax savings. For example, in Colorado contributions made to a CollegeInvest 529 account are deductible for state income tax purposes. By routing elementary and secondary school tuition payments through a 529 account, some of that tuition is effectively tax deductible for state income tax purposes. In Colorado this results in a savings of $463 each year if the full $10,000 is used. For families with multiple children the savings is multiplied accordingly as the $10,000 limitation appears to be a per-529 account limit, and not an overall family limitation.

Capital Gain On the Sale of a Principal Residence

The Proposal: The proposed legislation retains the $500,000 ($250,000 for unmarried taxpayers) capital gain exclusion on the sale of a primary residence. However, the proposed legislation would limit its availability. Currently, in order to qualify for the exclusion the home must be owned and used as a primary residence for two of the prior five tax years preceding the sale. The proposed legislation would require ownership and use of five of the prior eight years, and would phase out the exclusion when taxpayer AGI exceeds $250,000 ($500,000 for joint filers) over a three-year period.

Analysis: Obviously the increased ownership and use requirement and phase-out reduces the availability of this popular exclusion for many taxpayers. It will be interesting to see if this upsets members of the residential real estate industry and is seen as something that may suppress the residential real estate market when combined with the limitations placed on the deductibility of home mortgage interest.

Conversion of Traditional IRAs to Roth IRAs

The Proposal: The proposed legislation would repeal IRC § 408A(d)(6), which allows taxpayers to convert traditional IRAs to Roth IRAs. The repeal would be effective for years after 2017.

Analysis: Taxpayers may contribute pre-tax dollars to traditional IRAs, distributions from which are subject to taxation. On the other hand, contributions to Roth IRAs are made using after tax dollars, but distributions are generally tax-free. Conversions of traditional IRAs to Roth IRAs is often a useful tax planning technique. A potential repeal should have some taxpayers considering whether to make this conversion before the end of 2017.

Estate, Gift and Generation Skipping Transfer Taxes

The Proposal: Current law allows for a unified credit for each individual that effectively exempts $5.49 million ($5.6 in 2018) of value in wealth transfers from any combination of estate and gift taxes. The current maximum rate of tax for both taxes is 40%. A similar exemption amount and tax rate exists for the generation skipping transfer tax. The House bill increases the unified credit to $10 million per person (indexed for inflation) effective for gifts and the estates of decedents dying after December 31, 2017. The House bill also repeals the estate and generation skipping transfer taxes for estate of decedents dying and generation skipping gifts made after December 31, 2023.

For gifts made after December 31, 2023 the maximum gift tax rate is reduced from 40% to 35%, and a credit effectively exempts the first $10 million (indexed for inflation) of wealth transfers from the tax.

Analysis: The increased unified credit would exempt more estates from the estate and generation skipping transfer taxes. Because the repeal is not effective for 6 years taxpayers with estates in excess of the enlarged unified credit amount (or expected to exceed that amount) should not hesitate to engage in appropriate tax planning. This is not the first time the estate tax has been scheduled for repeal. Legislation enacted in 2001 called for the phase out and total repeal of the estate tax in 2010. Largely that did not occur, so I would be skeptical about a total repeal in 2023. The fact that the House GOP has not called for the immediate repeal of the estate tax also leads me to believe there may be more movement on this topic and any final legislation could be quite a bit different.

If the estate tax is repealed the tax free step-up in basis available with respect to property inherited which is retained insures that a tremendous amount of wealth conceivably passes to younger generations tax-free.

Unfortunately, a planned repeal to occur in several years is reminiscent of the situation estate planners faced from 2001 to nearly 2010 and complicated the estate plan process for many individuals.

Alternative Minimum Tax

The Proposal: Under the House bill the alternative minimum tax (AMT) would be repealed beginning in 2018. Taxpayers with AMT credit carryforwards would be able to claim a partial refund (50%) (to the extent credits exceed regular tax) in 2019, 2020 and 2021, and in 2022 the taxpayer could claim all remaining credits.

Analysis: Proposals to completely repeal the AMT are often discussed because this tax, which was originally intended to impact a small number of taxpayers, seems to potentially impact more taxpayers each year. Legislation is periodically passed to limit the application of this tax, but has never repealed it.

Tax Reform Affecting Businesses

Corporate Income Tax Rate

The Proposal: Beginning in 2018 the corporate tax rate is reduced from 35% to 20%, and the tax rate for personal service corporations is reduced to 25%.

Analysis: Perhaps the cornerstone of this legislation and a change championed by President Trump during his presidential campaign, this may also be the bill’s most controversial change. The 35% rate is among the highest corporate rates among developed countries, but the effective tax rate, calculated after taking into account available deductions, tax credits, etc. and as determined by the Congressional Budget Office is currently 18.6%, less than Japan and the U.K. and slightly higher than Germany (15.5%). Quantifying the effect of this change shouldn’t be done without regard to other changes to tax laws impacting corporations.

This change does not impact S corporations, limited liability companies, partnerships, and other flow-through business entities.

Tax Rate on Flow-Through Income (Business Income of Individuals)

The Proposal: Flow-through business entities (S corporations, limited liability companies, partnerships, etc.) are generally not subject to income and capital gains taxes. Instead, the owners of such entities recognize and pay tax on their share of business income and capital gains at the ordinary income and capital gain rates otherwise applicable to such persons.

The proposed change in the law creates what appears to be a somewhat complex structure for the taxation of such income. Beginning in 2018, the law would be changed to attempt to tax “qualified business income” at a maximum 25% rate. Flow-through income would be broken up into two categories, (1) “qualified business income,” and (2) wages. Two options allow taxpayers to elect how income is split among these categories. A first option splits total income among the business income and wage categories based upon a 30/70 split. The second option would split income based upon capital investment. For this second option, the “capital percentage” is equal to a “specified return on capital” divided by the taxpayer’s net business income derived from the business activity. The specified return on capital is the excess of (a) the product of the deemed rate of return and the asset balance, over (b) the interest paid or accrued and deductible. The “deemed rate of return” makes reference to a monthly interest rate regularly announced by the IRS, plus 7%. “Asset balance” means the adjusted basis of all assets used in the business activity.

Distributions from passive business activities would be treated as solely qualifying business income subject to the reduced rate.

The bill excludes professional service corporations (accountants, lawyers, engineers, physicians) from using the 30/70 formula. Because many of these business require little capital investment, the reduced rate may be effectively unavailable. However, if the business requires significant capital investments, such as some medical practices, the reduced tax rate may be available.

Analysis: There’s a lot to digest here. Months ago there were reports that drafters of tax legislation were having a difficult time how to draft laws allowing for a reduced tax rate on flow-through income that wasn’t potentially subject to “abuse” beyond the intended outcomes. This provision does little towards “simplifying” the tax code, and has the potential to provide a huge benefit to passive investors in business activities such as real estate development and ownership.

Interestingly, the bill does nothing to repeal the carried interest rules that both Pres. Trump and Hillary Clinton claimed would be repealed if either were elected president.

Increased Expensing

The Proposal: Businesses will be able to fully and immediately deduct the cost of depreciable assets (as opposed to depreciating those costs over the assets’ useful lives) with a maximum deduction of $5 million for the tax years 2018 through 2022. The maximum deduction is phased out to the extent acquisitions exceeds $20 million. The current limitation is $500,000 (and phase-out is $2 million).

Analysis: This popular expensing provision is designed to spur businesses towards increased capital investments.

Deductible Interest

The Proposal: Under the House bill businesses will only be able to deduct interest expense to the extent of 30% of adjusted taxable income, plus interest income (not applicable to banks). Businesses with gross receipts of $25 million or less are not subject to these rules.

Analysis: Under current law businesses may generally deduct all interest paid or accrued in a tax year. The inability to deduct all interest may impact how business choose to finance their operations (whether through debt or equity), and may make the analysis more difficult.

Section 1031 Like Kind Exchanges

The Proposal: Section 1031 of the Internal Revenue Code enables taxpayers to exchange property for other property of a “like-kind” without the recognition of taxable income. The proposed legislation would limit the applicability of Section 1031 to exchanges of real property only.

Analysis: Section 1031 is probably most often used in conjunction with the exchange of real property so this proposal may not change much for most taxpayers.

International Taxation

Participation Exemption for Foreign Income

The Proposal: The House bill creates a new participation exemption that effectively eliminates the tax on dividends paid by a foreign corporation to its U.S. corporate shareholder(s). To qualify for the participation exemption the U.S. shareholder must be a corporation and presumably (because the draft legislation is not entirely clear on this point) at least a 10% shareholder in the foreign corporation. Only that portion of dividends attributable to income from foreign sources is eligible to the participation exemption. The foreign tax credit would be disallowed with respect to foreign taxes attributable to such income.

To transition to the territorial system of tax 10% or greater U.S. shareholders in foreign corporations would be required to include in income for the subsidiary’s last tax year beginning before 2018 the shareholders pro rata portion of earnings and profits (post-1986) that has not been previously subject to U.S. tax. That portion of earnings and profits comprised of cash or cash equivalents would be taxed at a rate of 12%, while all other earnings and profits would be taxed at a rate of 5%. The U.S. shareholder could elect to pay such tax over a period of eight years in equal annual installments.

Analysis: Participation exemption systems have been used by other countries (the Netherlands is the first that comes to mind) for quite some time. Currently, the U.S. taxes its citizens, residents, and domestic business entities on their worldwide earnings, while much of the developed world has adopted a “territorial” system of taxation whereby each country taxes only the income derived from within its borders. The U.S. relies on tax treaties and a foreign tax credit to insure U.S. persons avoid the double taxation of income (in this case, taxing the same income more than once by multiple jurisdictions). For years many tax professionals and members of the business community have been urging the U.S. to move towards a system of territorial taxation. This proposal endeavors to do that.

During his campaign President Trump indicated a desire to change the tax laws so that U.S. corporations with large cash positions in foreign subsidiaries would repatriate some of those earnings. This proposal should make it easier for these U.S. based multinationals to bring that cash back home.

Indirect Foreign Tax Credits

The Proposal: The indirect foreign tax credit would be repealed under the House GOP bill with respect to taxes attributable to income qualifying for the participation exemption. The indirect foreign tax credit is available to certain U.S. corporations that own stock in foreign corporations, and such stockholdings satisfy certain ownership criteria (generally with regard to the percentage of the subsidiary owned). Upon repatriation of profits (the payment of dividends to the U.S. parent, the parent is able to claim a foreign tax credit attributable to foreign taxes paid by the foreign subsidiary on its earnings.

Analysis: The participation exemption would seemingly make the indirect foreign tax credit unnecessary.

Changes to Subpart F

The Proposal: Subpart F refers to that portion of the Internal Revenue Code containing a set of rules used to curb the deferral of U.S. income tax on certain forms of foreign income earned by foreign corporations controlled by U.S. shareholders. The proposed legislation makes several modifications to Subpart F including indexing for inflation the de minimis exception to foreign base company income, making permanent the “look-through” rule regarding related foreign corporations, modifying the constructive ownership rules, and eliminating the requirement that a CFC (controlled foreign corporation) must be controlled by U.S. persons for at least 30 days during a tax year.

Analysis: Most Americans won’t be impacted by these rules. The most significant change might be the elimination of the 30-day requirement, which could result in more taxpayers having to recognize and pay tax on foreign source income.

Prevention of Base Erosion

The Proposal: Base erosion refers to the general strategy of exploiting differences in tax rules among countries to artificially shift profits to low-tax or no-tax jurisdictions. The proposed legislation takes several steps designed to curb the ability of taxpayers to avoid U.S. tax by artificially shifting income to other jurisdictions.

The legislation calls for the recognition of income equal to 50% of a CFC’s high return income by a U.S. shareholder. This somewhat complex calculation of high return income appears to target income beyond a threshold amount (determined with reference to an assumed rate of return based upon monthly applicable federal rates reported by the IRS) that would otherwise escape U.S. taxation.

A new excise tax of 20% would also be imposed on payments made by a U.S. corporation to a related foreign corporation, unless the foreign corporation elects to treat such income as effectively connected with a U.S. trade or business (in which case such income would be subject to U.S. taxation).

Analysis: Internationally many countries are trying to combat base erosion and eliminate the benefits of artificially shifting income to tax havens. The proposed legislation appears to go a long way in addressing these concerns. Requiring the recognition of high return income seems a bit arbitrary at first glance, while the excise tax on payments to related foreign persons may survive to final legislation. In all cases, these reforms are most likely limited in application to multinational corporations.